Rental DSCR Loans

- Dedicated Client Support

- Competitive Rates & Terms

- Tailored Financial Solutions

- Fast & Easy Application Process

- Access to a Broad Lender Network

- Financial Expertise You Can Trust

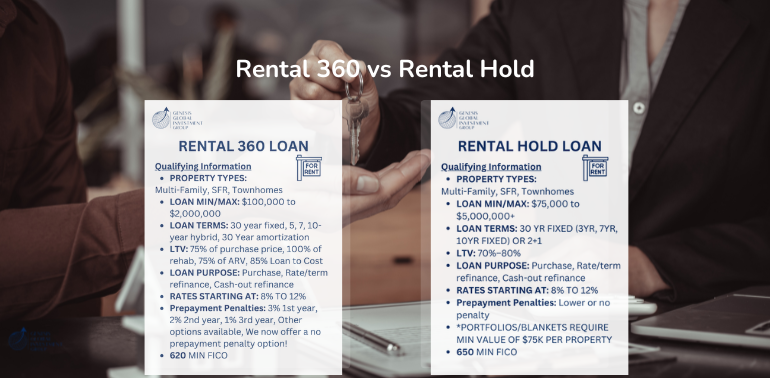

Two Types of DSCR Loans: Rental 360 vs. Rental Hold

Debt-Service Coverage Ratio (DSCR) loans are designed for real estate investors who want financing based on rental income rather than personal income. Two popular DSCR loan options are Rental 360 and Rental Hold. Both cater to rental property investors but differ in terms, flexibility, and long-term benefits.

1. Rental 360 Loan (Traditional Long-Term DSCR Loan)

Best for: Investors seeking a fixed, long-term mortgage with predictable payments. Loan Term: 30-year fully amortizing (fixed-rate or adjustable-rate options). DSCR Requirement: Typically 1.0–1.25 (rental income must cover mortgage payments). Loan-to-Value (LTV): Up to 80% (purchase & refinance), 75% (cash-out refinance). Prepayment Penalty: May apply (3–5 years, depending on lender). Property Types: Single-family, 2-4 unit, multifamily (5+ units), mixed-use properties. Borrower Structure: Can be under LLC, corporation, or individual name. Cash-Out Option: Available for reinvestment, debt consolidation, or property improvements. Closing Time: 21–45 days.

Best for: Investors seeking a fixed, long-term mortgage with predictable payments. Loan Term: 30-year fully amortizing (fixed-rate or adjustable-rate options). DSCR Requirement: Typically 1.0–1.25 (rental income must cover mortgage payments). Loan-to-Value (LTV): Up to 80% (purchase & refinance), 75% (cash-out refinance). Prepayment Penalty: May apply (3–5 years, depending on lender). Property Types: Single-family, 2-4 unit, multifamily (5+ units), mixed-use properties. Borrower Structure: Can be under LLC, corporation, or individual name. Cash-Out Option: Available for reinvestment, debt consolidation, or property improvements. Closing Time: 21–45 days.

Key Benefit:

Long-term financing stability with a 30-year loan term, making it ideal for buy-and-hold investors focused on consistent rental income and property appreciation.

2. Rental Hold Loan (Short-Term, Flexible DSCR Loan)

Best for: Investors looking for short-term financing before refinancing or selling. Loan Term: 5–10 years, with interest-only or amortizing payment options. DSCR Requirement: More flexible (as low as 0.75–1.0 DSCR in some cases). Loan-to-Value (LTV): Usually up to 75%–80%. Prepayment Penalty: Typically lower than Rental 360, allowing faster exit strategies. Property Types: Similar to Rental 360, including single-family, multifamily, and mixed-use properties. Borrower Structure: Usually structured under LLCs or corporations for investors planning short-term strategies. Cash-Out Option: Available but may have different terms compared to Rental 360. Closing Time: Often faster than Rental 360, typically 15–30 days.

Key Benefit:

Shorter loan term with flexible exit options, making it ideal for investors who plan to refinance, sell, or transition properties within a few years.

Which One Is Right for You?

| Feature | Rental 360 (Long-Term) | Rental Hold (Short-Term) |

|---|---|---|

| Best for | Buy-and-hold investors | Short-term investors |

| Loan Term | 30 year fixed, 5, 7, 10-year hybrid, 30 Year amortization (fixed/adjustable) | 30yr Fixed (3yr, 7yr 10yr Fixed) OR 2+1 (interest-only options) |

| DSCR Requirement | 1.0–1.25 | 1.0–1.25 |

| LTV (Max.) | 85% purchase/refi, 75% cash-out | 70%–80% |

| Prepayment Penalty | 3% 1st year, 2% 2nd year, 1% 3rd year, | Lower or no penalty |

| Property Types | SFR, multifamily, mixed-use | SFR, multifamily, mixed-use |

| Closing Time | 21–45 days | 15–30 days |

| Exit Strategy | Long-term hold | Refinance, sell, or reposition property |

Final Thought:

Choose Rental 360 if you want long-term stability, predictable payments, and cash flow-focused financing.

Choose Rental Hold if you need flexibility for short-term strategies like repositioning, refinancing, or selling properties.